This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For retail executives, finding ways to reduce these processing fees is crucial to improving profit margins and staying competitive in todays increasingly cashless economy. However, the complex and often unclear credit card processing system can make this difficult. Manage chargebacks effectively.

They extend to things like livestreams, shoppable content and payment links within Instagram Reels, stories, TikTok videos or Pinterest Pins. Here, Ill outline this infrastructure and other top considerations for merchants and platforms as they wade into this new domain.

The adoption of cryptocurrencies has expanded beyond investment and trading, with businesses worldwide integrating crypto payment gateways into their operations. A crypto payment gateway allows merchants to accept cryptocurrency payments from customers, offering an alternative to traditional fiat transactions.

The challenging economic environment, intense regulatory pressure and ever-present threat of fraud are creating a perfect storm that’s sweeping across the global payments landscape. Instead of seeing compliance as a painful obligation, it’s time to see it as a springboard for innovation, expansion and collaboration.

The seamless nature of digital commerce has inspired consumers to expect more from the payment experience everywhere they shop — online, in-store and even via social channels. Customers today expect to be able to shop where and when they want and use the payment method they want.” more compared to their previous buying levels.

That inherent distaste for the transaction phase is one reason payment companies are so eager to expand into other parts of the shopper journey. Embedded finance has become big business: McKinsey estimated that the sector reached $20 billion in revenue in the U.S. Denise Leonhard, VP and GM, Venmo.

The Reserve Bank of Australia (RBA) says it will “revisit” the issue of surcharging in the buy now, pay later (BNPL) sector, flagging a new review to assess if payment sector reforms are necessary. The review will focus on surcharging, Connolly said, given the rapid development of payment systems available to merchants and consumers. “The

In recent years, cryptocurrencies have emerged as a transformative force in the world of finance. As their popularity continues to surge, it is crucial for retailers to consider embracing crypto acceptance as a payment option. There are a number of businesses across Australia already accepting cryptocurrency payments.

As economic pressures and living costs surge, more people than ever are considering using point-of-service (POS) finance — such as buy now, pay later and installment loans — to manage their cashflow. It’s clear that there is a consumer-driven need for more flexible finance and smarter buying power. .

In addition to the products and services they offer, retailers are reconsidering the environmental and social impacts of their supply chains, employee activity and even which partners they choose to work with in an effort to fulfill a moral obligation to their consumers — especially the younger generation.

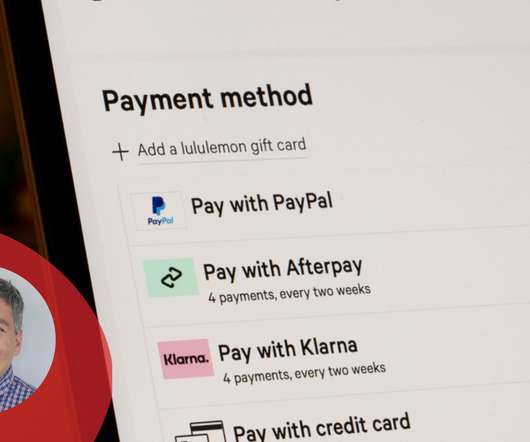

consumers have now used a buy now pay later (BNPL) service. . Businesses looking for ways to gain a competitive edge over their competitors have been pushing service advantages into new areas, including alternative payment models. Using BNPL, approved customers can defer payments at checkout — both online and in-store.

The good news is that since its global popularization in 2020, Buy Now Pay Later (BNPL) has become a real game-changer for merchants looking to boost their business. For shoppers, BNPL is a seamless payment method that helps break up their purchases into several installments, bringing more cash flow and budgeting flexibility.

Same goes for the services Alibaba is building to stay competitive: financing solutions, fulfillment services, AI tools to make the process of using the platform easier, localized warehousing to speed up delivery. In operation since 1999, Alibaba.com currently serves approximately 8 million SMEs in the U.S

The Melbourne, Australia-based company currently serves more than 16 million consumers and nearly 100,000 merchants worldwide. Payment industry experts see the acquisition as a win for both companies as well as a sign of the growing ubiquity of BNPL. Schwartz noted that Afterpay is a founding member of the CLA’s BNPL task force.

So far, this payment method has made it easy for millions to purchase nice-to-have items such as the latest iPhone, trendy sofas, designer handbags and stylish clothes without paying in full upfront. However, hidden fees and late payment penalties can seriously damage consumers’ financial well-being as they can easily rack up massive debt.

It’s clear this reverse layaway payment model is also here to stay. In BNPL, consumers receive the goods or services that they want to buy, but payment is staggered over monthly payments for a certain period of time with no interest. But as stand-alone BNPL apps continue to grow, so will the threats against them.

The economic fallout from the COVID-19 pandemic accelerated demand for buy now, pay later (BNPL) payment options. Research by The Ascent showed that among people who have used a BNPL service, 45% first did so in 2019, 21% first did so in 2020, and only 7% had used a BNPL service prior to 2015. billion, according to IBISWorld.

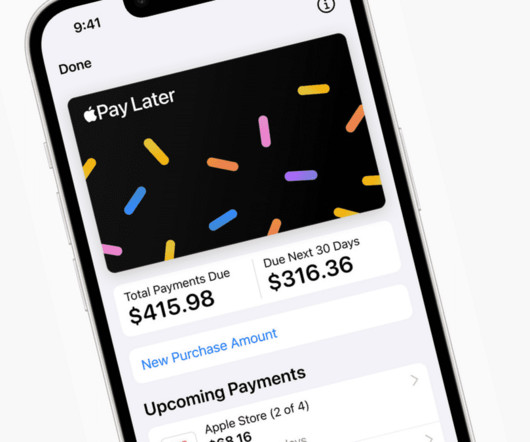

Pay Later — which will let users split purchases into four payments spread over six weeks with no interest and no fees — is now available for some randomly selected Apple Wallet users in the U.S., Before a payment is due, users also will receive notifications via Wallet and email. and will roll out to all users in the coming months.

Because of this ease, merchants have begun relying on POS financing to drive sales growth. McKinsey has found that around 50% to 60% of loans originated at POS are either partially or entirely subsidized by the merchant. According to McKinsey, merchants face up to 2.4X Penalties for exceeding fraud thresholds.

Axerve, Payment Partner to Grow, specialising in creating accessible and frictionless payment solutions for Ecommerce and physical sales, today announces the release of a new white paper, ‘ New technologies and trends in digital payments in 2022 ’. Payment orchestration is a key tool for managing this increased complexity.

PayPal Holdings Inc’s new “buy now, pay later” offering in Australia will not charge late payment fees, the U.S. payments giant said on Wednesday, as it attempts to edge past main industry rival Afterpay in the country. It, however, lets the merchants set their own minimum spend value.

They want shopping to be fast and fun — less of a process. That’s why Synchrony partnered with payments startup Skipify, which enables purchases instantly across email, text, social and other channels. Merchants who break out of the old way of doing things will be perfectly positioned to profit for years to come. .

The industry’s latest move: accepting cryptocurrency as a form of payment. In countries where crypto is more regulated, retailers have opted to join forces with licensed payment platforms that are registered with local finance institutions to process transactions. Beyond payment.

Most buy now, pay later offers are interest- and fee-free, unless customers miss a payment. consumers say they have used a buy now, pay later service, according to a recent study from The Ascent, a Motley Fool service. In fact, 50% of U.S The Appeal of BNPL: Layaway Without the Stigma.

The acceptance of cash has started to trend upwards again, but payment technology is helping businesses to deliver consistently better experiences, so what does the future hold? And how can businesses be ready for evolving payment technologies? Consumers, too, preferred to use contactless payments or to shop online.

But the payment method is already truly embedded in the digital economy and is not going anywhere, even if it is regulated. Let’s look at the conditions that were so favourable to this payment method, the inevitable regulations and consumer and media response. BNPL is disrupting credit and driving competition.

Speaking to merchants in Australia, it’s clear that the retail landscape is more competitive than ever, intensified by the influx of global e-commerce players and price-conscious consumers. Improve operational efficiency Business efficiency issues are a big pain point for many Australian retailers.

If you’re like most small business owners, you’re always on the lookout for new small business financing options. In this article, we’ll explore 20 different financing options for small businesses such as traditional bank loans. What is Business Financing? Three Main Types of Financing for Businesses.

Signifyd has received $205 million in Series E growth equity financing that values the company at $1.34 The funding will be used to expand the Signifyd Commerce Protection Platform and identity graph globally across digital shopping and payments.

The issue for so many of these companies might have been that the move to e-tail from retail meant giving up their own brand and an experience their customers love, and joining up with one of these giants as a nameless, faceless merchant amidst a sea of millions.

NatWest Group has signed agreements with three payment providers – TrueLayer, GoCardless and Crezco – to offer Variable Recurring Payments (VRP) as a new and convenient payment option for businesses and consumers.

For retailers looking to expand their operations, securing financing is a crucial step to fuel growth. Financing this growth remains a significant challenge for many retailers, from small boutiques to large chains. Financing this growth remains a significant challenge for many retailers, from small boutiques to large chains.

A point-of-sale system is one of the best tools for small businesses looking to accept payments. Point-of-sale systems enable business owners to be more agile with their paymentprocessing and forego using the cash drawer. A point of sale (POS) system is used to accept payments, like a cash register. Brilliant POS.

The holidays always tend to put a strain on the piggy bank, but a study from personal finance company Credit Karma found that 43% of consumers are feeling more financially stressed this holiday season, and inflation is the leading cause. Even outside of the holiday season, uptake in buy now, pay later (BNPL) services is exploding in the U.S.,

If you’re also struggling to stay afloat due to piled-up accounts receivable, you can opt for accounts receivable financing to improve cash flow in your company. What Is Accounts Receivable Financing? Accounts receivable financing should not be confused with invoice factoring. How Does Accounts Receivable Financing Work?

The platform now features more than 100,000 brands from 100 + countries, and in September 2023, ecommerce vanguard Shopify took a stake in the company and made Faire the recommended wholesale marketplace for its millions of merchants. The innovation that we at Faire brought to the market was offering free returns and net-60 payment terms.

In February, ShopBack, a shopping, rewards and payments platform, partnered with Sunway Pyramid, a mall in Malaysia, on the ShopFiesta event to reward shoppers with promotions and giveaways. Shoppers were able to make purchases at a discount and split their payments into three instalments. It was all about boosting in-store shopping.

New customers are a major growth engine for retailers, but many merchants view first-time online shoppers as high-risk due to their unfamiliar behaviour and lack of purchase history. Our data already shows that across the e-commerce landscape, up to 70 per cent of orders that are declined by merchants are made by legitimate customers.

With Christmas just around the corner, it’s important to stay vigilant as scams and fraud can happen to any business that accepts debit and credit card payments, and can have a significant financial and reputational impact at this time of year. Tools like 3DSecure can help with these additional security processes.

Super apps in Asia are trendy, and with good reason: they gather together a number of essential everyday services onto a single, easy-to-use platform. Sea, for example, provides an integrated suite of e-commerce (through Shopee), digital entertainment and financial services. Financial services accounted for $412.8

Shopback’s decision to terminate its buy now pay later (BNPL) service in Malaysia and Singapore has sparked discussions and raised pertinent questions about the future of digital payment solutions in the region. According to a statutory declaration, Pace was unable to continue business operations “by reason of its liabilities”.

Believe it or not, merchant cash advance (MCA) business loans are a great option for small business owners looking for fast and easy access to capital. They’re an ideal financing solution for companies that have been denied a traditional bank loan or don’t have the time to wait around for a business loan approval.

A new study from FIS ® (NYSE: FIS), shows how the shopping preferences of younger UK consumers have shifted as adoption of embedded financeservices reaches mainstream usage among Millennials and Gen Zs, while their older counterparts are less engaged with newer, digitally-oriented financial experiences.

Online shoppers may find they need to confirm their identity more often when making payments from Monday, as changes to combat fraud come into force. She continued: “When a customer makes a payment online, their bank or payment provider will need to verify who they are before the transaction will go through.

We organize all of the trending information in your field so you don't have to. Join 40,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content