This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

They extend to things like livestreams, shoppable content and payment links within Instagram Reels, stories, TikTok videos or Pinterest Pins. Whats more, Deloitte data shows that consumers using social media were four times more likely to add more to their baskets or make purchases of a higher value than they would when shopping off-channel.

The adoption of cryptocurrencies has expanded beyond investment and trading, with businesses worldwide integrating crypto payment gateways into their operations. A crypto payment gateway allows merchants to accept cryptocurrency payments from customers, offering an alternative to traditional fiat transactions.

If we thought the pandemic-driven shift to digital payments was an evolution, we’re about to be catapulted into a new world, where payments will become possible in places thought impossible just a few years ago. In fact, embedded finance will be a $777 billion opportunity by 2029. So how can businesses get a piece of it?

Over the past decade, the payments environment has experienced significant upheaval, driven by swift technical improvements. Innovations such as contactless cards, mobile wallets, blockchain, and real-time payments are transforming transaction methods for consumers and companies.

The challenging economic environment, intense regulatory pressure and ever-present threat of fraud are creating a perfect storm that’s sweeping across the global payments landscape. Instead of seeing compliance as a painful obligation, it’s time to see it as a springboard for innovation, expansion and collaboration.

This includes enhancing in-store inventory, delivery services and even the personalization of customer service. However, when it’s time to check out, how do payment options factor into that customer experience? Is it Great Service or Great Financing Options? It goes without saying that great service is important.

The automotive industry is undergoing a profound transformation, driven by the integration of financial technology (FinTech) into car finance options. This shift not only enhances the purchasing experience for consumers but also streamlines processes for dealerships and financial institutions.

The seamless nature of digital commerce has inspired consumers to expect more from the payment experience everywhere they shop — online, in-store and even via social channels. Customers today expect to be able to shop where and when they want and use the payment method they want.” more compared to their previous buying levels.

For me, the great thing about working in finance is getting to make decisions that touch all aspects of the organization. Finance really places you at the center of everything, where decisions you make play a pivotal role in sustaining long-term business success. That is, at least, the theory. But it doesn’t have to be this way.

The Federal Court has ruled that Harvey Norman, along with Latitude Finance Australia, made false and misleading financial claims in a national advertising campaign. The campaign, which ran from January 2020 to August 2021, was for a 60-month interest-free and no-deposit payment method.

Accusations of “greenwashing” can lead to irreversible damage to reputation and consumer trust, and with environmental social governance (ESG) now high on the agenda for public and private organizations worldwide, it’s changing how many retailers think about their businesses. And how can POS finance fit into the equation?

Businesses today operate in a fast-moving cyber threat landscape. As digital operations become more complex and cybercriminals launch increasingly sophisticated phishing and malware attacks, data breaches have become common occurrences. For retailers and consumer businesses, a surge in data breaches presents difficult challenges.

That inherent distaste for the transaction phase is one reason payment companies are so eager to expand into other parts of the shopper journey. Embedded finance has become big business: McKinsey estimated that the sector reached $20 billion in revenue in the U.S. Denise Leonhard, VP and GM, Venmo.

These devices, like smart doorbells, thermostats, lighting and more, present an exciting opportunity for retailers, but understanding consumers motivations and proactively addressing potential concerns will be vital to make the most of this dynamic market. Craig Thole is SVP of Emerging Solutions, Global Connected Living, at Assurant, Inc.

In recent years, cryptocurrencies have emerged as a transformative force in the world of finance. As their popularity continues to surge, it is crucial for retailers to consider embracing crypto acceptance as a payment option. There are a number of businesses across Australia already accepting cryptocurrency payments.

As economic pressures and living costs surge, more people than ever are considering using point-of-service (POS) finance — such as buy now, pay later and installment loans — to manage their cashflow. It’s clear that there is a consumer-driven need for more flexible finance and smarter buying power. .

Apple Pay, Google Pay and China’s WeChat Pay, which have grown rapidly in recent years, are not currently designated as payment systems, putting them outside Australia’s financial regulatory system. It would also give powers to the treasurer to order regulators to check if any payment platforms pose risks to the country.

Throughout the past few pandemic years, buy now, pay later (BNPL) has become the latest fintech trend to change how people pay for goods and services. A majority of American consumers have now used a BNPL service, up from 37.65% in July of 2020 — an increase of almost 50% in less than one year. Meeting B2B Business Needs.

Options such as buy now, pay later (BNPL) services were first introduced to business to consumer (B2C) transactions, giving customers the ability to access products and services they need today while paying at a later date or over a series of instalments. . Transform your B2B transactions with better payment technology.

Consumers are quickly losing trust, and companies must act swiftly and responsibly to restore it. A Pew Research study reveals a concerning trend: 67% of consumers have little understanding of what companies do with their data, a sentiment echoed by an IAPP study which found that only 29% feel informed about how their data is protected.

million debt servicepayment on municipal bonds sold to help finance the venture, due to insufficient funds. The mall also had missed the previous payment deadline for the same reason in August 2022. featuring styles appropriate for Islamic and other religious consumers). 1, 2023 $8.8 The notice from U.S.

Same goes for the services Alibaba is building to stay competitive: financing solutions, fulfillment services, AI tools to make the process of using the platform easier, localized warehousing to speed up delivery. In operation since 1999, Alibaba.com currently serves approximately 8 million SMEs in the U.S

Buy now pay later (BNPL) services have quickly become commonplace for consumers. Offering people the ability to spread out their payments for goods and services across regular intervals enables consumers to better manage their own cash flow. Shift the financial risk with third-party business finance.

Providing healthcare services — such as Botox, hair removal, skin contouring and even facelifts — in a sleek spa environment means many who first come in for a one-time facial or massage ultimately may opt for more expensive healthcare services. What’s fueling this growing phenomenon?

And it’s increasingly clear that brands that embrace financial services within the customer journey are scoring highly on engagement scores. What’s more, the number of payment providers on the market has dramatically multiplied over the years, creating a vast and often confusing ecosystem. It’s reckoned that nearly 4.5

While many have seen the words “Web 3.0,” “blockchain” and even NFTs in the headlines, there is still more to learn about these topics and the overall decentralized finance (DeFi) space. The agenda is designed to hit on all the core issues surrounding this space, from cybersecurity to finance and customer experience.

Economic and demographic drivers The General Statistics Office of Vietnam estimated retail sales of goods and consumerservices grew by 9.3 Previously, many Vietnamese consumers preferred shopping abroad, especially in Bangkok, due to the strong presence of international brands. per cent year-on-year in Q4 last year.

With retailers already pushing out holiday sales to entice consumers to buy early and avoid delivery delays due to supply chain congestion, one tactic that they will lean on to entice customers is buy now, pay later (BNPL). BNPL Can Have an Effect on Consumers and Retailers.

The Reserve Bank of Australia (RBA) says it will “revisit” the issue of surcharging in the buy now, pay later (BNPL) sector, flagging a new review to assess if payment sector reforms are necessary. The review will focus on surcharging, Connolly said, given the rapid development of payment systems available to merchants and consumers.

For shoppers, BNPL is a seamless payment method that helps break up their purchases into several installments, bringing more cash flow and budgeting flexibility. Customers that have a positive point-of-sale financing experience are more likely to repeat purchases from that retail brand if the BNPL option is white-labeled for the retailer.

Over the years the retailer has carved a unique space in the Hispanic market thanks to its unique approach to financing, in-store services and merchandising. The core business was always built [around] providing dignified credit, because consumers couldn’t buy items outright with cash. population.

In today’s digital-first marketplace, consumer expectations for flawless shopping experiences, whether in-store or online, have reached unprecedented heights and are putting pressure on retailers to provide an “always on” business model. Months earlier, it was reported that thousands of Walmart stores in the U.S.

So far, this payment method has made it easy for millions to purchase nice-to-have items such as the latest iPhone, trendy sofas, designer handbags and stylish clothes without paying in full upfront. However, hidden fees and late payment penalties can seriously damage consumers’ financial well-being as they can easily rack up massive debt.

Humans have been dynamically evolving the concept of loans and credit in commerce for hundreds of years — culminating in the explosion of consumer credit cards in the 20th century. consumers have now used a buy now pay later (BNPL) service. . consumers have now used a buy now pay later (BNPL) service. .

They want shopping to be fast and fun — less of a process. That’s why Synchrony partnered with payments startup Skipify, which enables purchases instantly across email, text, social and other channels. But an online presence is necessary, as consumers typically research and review before purchasing.

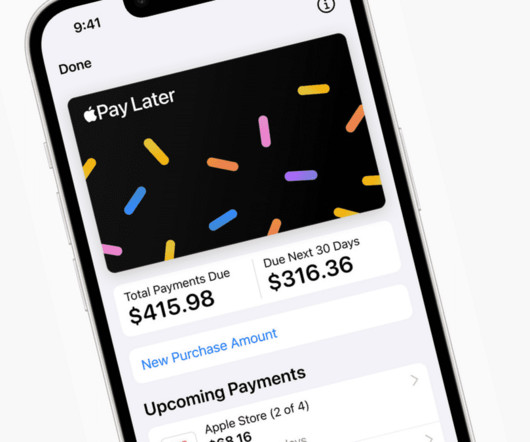

Pay Later — which will let users split purchases into four payments spread over six weeks with no interest and no fees — is now available for some randomly selected Apple Wallet users in the U.S., Before a payment is due, users also will receive notifications via Wallet and email. and will roll out to all users in the coming months.

And thanks to a seamless payment experience powered by SplitIt , GSN is creating inspiring content about its fine jewelry and is then translating it into bottom-line results. “If Since launching the partnership in 2021, GSN has processed about 9,000 transactions using SplitIt, totaling more than $30 million in sales.

The Melbourne, Australia-based company currently serves more than 16 million consumers and nearly 100,000 merchants worldwide. Payment industry experts see the acquisition as a win for both companies as well as a sign of the growing ubiquity of BNPL. Schwartz noted that Afterpay is a founding member of the CLA’s BNPL task force.

Which is great news for consumers who are unabashed fans of buy now, pay later, also called BNPL. Buy now, pay later is short-term financing that allows people to buy everyday items like home goods, electronics and clothes in low to no interest monthly installments — and receive the goods immediately. It’s just…delayed gratification.

A car is one of the biggest purchases most consumers make, but the process of buying one, especially used, has long been one of consumers’ most dreaded retail experiences. From the moment it debuted in 1993, CarMax set out to change that with a focus on honest sales interactions and simplified processes.

The Retail Food Group (RFG) will pay $5 million to some franchisees of Michel Patisserie stores as part of a court-enforceable undertaking that settles the unconscionable conduct proceedings brought by the Australian Competition and Consumer Commission (ACCC). Michel’s marketing fund. Waiving historical debts.

The Retail Food Group (RFG) will pay $5 million to some franchisees of Michel Patisserie stores as part of a court-enforceable undertaking that settles the unconscionable conduct proceedings brought by the Australian Competition and Consumer Commission (ACCC). Michel’s marketing fund. Waiving historical debts.

The automotive industry is undergoing a profound transformation, driven by the integration of financial technology (FinTech) into car finance options. This shift not only enhances the purchasing experience for consumers but also streamlines processes for dealerships and financial institutions.

Despite having just officially begun, this holiday shopping season already is marked by supply chain disruption, persistent inflation and mixed consumer confidence. And just like last year, it looks like consumers will respond by turning to ecommerce. Shortages and Sticker Shock Heighten Holiday Stress.

We organize all of the trending information in your field so you don't have to. Join 40,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content