This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

They extend to things like livestreams, shoppable content and payment links within Instagram Reels, stories, TikTok videos or Pinterest Pins. Whats more, Deloitte data shows that consumers using social media were four times more likely to add more to their baskets or make purchases of a higher value than they would when shopping off-channel.

The adoption of cryptocurrencies has expanded beyond investment and trading, with businesses worldwide integrating crypto payment gateways into their operations. A crypto payment gateway allows merchants to accept cryptocurrency payments from customers, offering an alternative to traditional fiat transactions.

The challenging economic environment, intense regulatory pressure and ever-present threat of fraud are creating a perfect storm that’s sweeping across the global payments landscape. Instead of seeing compliance as a painful obligation, it’s time to see it as a springboard for innovation, expansion and collaboration.

The Reserve Bank of Australia (RBA) says it will “revisit” the issue of surcharging in the buy now, pay later (BNPL) sector, flagging a new review to assess if payment sector reforms are necessary. The review will focus on surcharging, Connolly said, given the rapid development of payment systems available to merchants and consumers. “The

As economic pressures and living costs surge, more people than ever are considering using point-of-service (POS) finance — such as buy now, pay later and installment loans — to manage their cashflow. It’s clear that there is a consumer-driven need for more flexible finance and smarter buying power. .

The seamless nature of digital commerce has inspired consumers to expect more from the payment experience everywhere they shop — online, in-store and even via social channels. Customers today expect to be able to shop where and when they want and use the payment method they want.” more compared to their previous buying levels.

That inherent distaste for the transaction phase is one reason payment companies are so eager to expand into other parts of the shopper journey. Embedded finance has become big business: McKinsey estimated that the sector reached $20 billion in revenue in the U.S. Denise Leonhard, VP and GM, Venmo.

Accusations of “greenwashing” can lead to irreversible damage to reputation and consumer trust, and with environmental social governance (ESG) now high on the agenda for public and private organizations worldwide, it’s changing how many retailers think about their businesses. And how can POS finance fit into the equation?

Amid all the ongoing furor around new artificial intelligence applications, when it comes to actual utility for both brands and consumers, the cream that has risen to the top appears to be AI-powered agents. This shift could eliminate the gap between research and purchase entirely, creating a more intuitive consumer journey.

The good news is that since its global popularization in 2020, Buy Now Pay Later (BNPL) has become a real game-changer for merchants looking to boost their business. For shoppers, BNPL is a seamless payment method that helps break up their purchases into several installments, bringing more cash flow and budgeting flexibility.

The Melbourne, Australia-based company currently serves more than 16 million consumers and nearly 100,000 merchants worldwide. Payment industry experts see the acquisition as a win for both companies as well as a sign of the growing ubiquity of BNPL. Schwartz noted that Afterpay is a founding member of the CLA’s BNPL task force.

So far, this payment method has made it easy for millions to purchase nice-to-have items such as the latest iPhone, trendy sofas, designer handbags and stylish clothes without paying in full upfront. However, hidden fees and late payment penalties can seriously damage consumers’ financial well-being as they can easily rack up massive debt.

Humans have been dynamically evolving the concept of loans and credit in commerce for hundreds of years — culminating in the explosion of consumer credit cards in the 20th century. consumers have now used a buy now pay later (BNPL) service. . consumers have now used a buy now pay later (BNPL) service. .

Same goes for the services Alibaba is building to stay competitive: financing solutions, fulfillment services, AI tools to make the process of using the platform easier, localized warehousing to speed up delivery. Sounds familiar, right? That’s because Amazon, and now Walmart, have all done the same.

In recent years, cryptocurrencies have emerged as a transformative force in the world of finance. As their popularity continues to surge, it is crucial for retailers to consider embracing crypto acceptance as a payment option. There are a number of businesses across Australia already accepting cryptocurrency payments.

The economic fallout from the COVID-19 pandemic accelerated demand for buy now, pay later (BNPL) payment options. Research by The Ascent showed that among people who have used a BNPL service, 45% first did so in 2019, 21% first did so in 2020, and only 7% had used a BNPL service prior to 2015. billion, according to IBISWorld.

Consumer preference for online shopping continues to rise, as more purchases are being made online than in stores with each passing year. Because of this ease, merchants have begun relying on POS financing to drive sales growth. According to McKinsey, merchants face up to 2.4X Penalties for exceeding fraud thresholds.

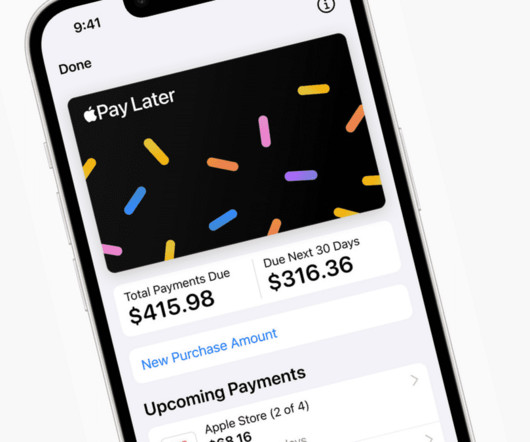

Pay Later — which will let users split purchases into four payments spread over six weeks with no interest and no fees — is now available for some randomly selected Apple Wallet users in the U.S., Before a payment is due, users also will receive notifications via Wallet and email. and will roll out to all users in the coming months.

They want shopping to be fast and fun — less of a process. That’s why Synchrony partnered with payments startup Skipify, which enables purchases instantly across email, text, social and other channels. But an online presence is necessary, as consumers typically research and review before purchasing.

It’s clear this reverse layaway payment model is also here to stay. In BNPL, consumers receive the goods or services that they want to buy, but payment is staggered over monthly payments for a certain period of time with no interest. It’s not hard to understand the appeal.

PayPal Holdings Inc’s new “buy now, pay later” offering in Australia will not charge late payment fees, the U.S. payments giant said on Wednesday, as it attempts to edge past main industry rival Afterpay in the country. It, however, lets the merchants set their own minimum spend value.

Despite having just officially begun, this holiday shopping season already is marked by supply chain disruption, persistent inflation and mixed consumer confidence. And just like last year, it looks like consumers will respond by turning to ecommerce. Shortages and Sticker Shock Heighten Holiday Stress.

But now, as BNPL offerings — and consumers’ understanding of them — mature, the explosive growth of the last two years is slowing. With inflation and interest rates on the rise, a more nuanced approach to BNPL is emerging, and experts say that’s a good thing for both consumers and retailers. In fact, 50% of U.S

Axerve, Payment Partner to Grow, specialising in creating accessible and frictionless payment solutions for Ecommerce and physical sales, today announces the release of a new white paper, ‘ New technologies and trends in digital payments in 2022 ’. Payment orchestration is a key tool for managing this increased complexity.

Last year, consumers reported spending more than $23 billion shopping small on Small Business Saturday, and we want to exceed that in 2022.”. It will integrate directly with Square’s solution ecosystem, empowering sellers to organize their finances and manage cash flow from the same platform they use to run their business.

Speaking to merchants in Australia, it’s clear that the retail landscape is more competitive than ever, intensified by the influx of global e-commerce players and price-conscious consumers. This also allowed it to offer ship-to-customer services to sell items that were available online but not held in store.

This adds up to a new outlook on finances for Gen Zers who are already taking a more careful approach in how, when and where they spend. More consumers today are discovering brands and products on social platforms, which makes omnichannel marketing so critical. Unlike other generations, Gen Zers expect flexibility in payments.

But the payment method is already truly embedded in the digital economy and is not going anywhere, even if it is regulated. Let’s look at the conditions that were so favourable to this payment method, the inevitable regulations and consumer and media response. BNPL is disrupting credit and driving competition.

The acceptance of cash has started to trend upwards again, but payment technology is helping businesses to deliver consistently better experiences, so what does the future hold? And how can businesses be ready for evolving payment technologies? Consumers, too, preferred to use contactless payments or to shop online.

It would seem that scales have long been tipped in favor of the retail giants — those with massive footprints, established brands, warehouses chock-full of supply to meet global consumer demand and the resources to offer a wide array of products. That reality is likely one reason why Amazon controls nearly 50% of all U.S. e-Commerce.

“There are three major players in the retail industry — the brands that make the products, the retailers that sell the products and the consumer who buys from the retailer,” said Max Rhodes, Co-founder and CEO of B2B marketplace Fa i re. The innovation that we at Faire brought to the market was offering free returns and net-60 payment terms.

Learning to master your inventory management processes can net significant bottom-line results in your ecommerce business. Inefficient processes and software: Not harnessing the right tools. If your ecommerce business has been around for a while, you might still be processing orders or managing your inventory with manual methods.

As a result, retailers are experiencing a daunting dilemma: to choose between absorbing cost increases or to pass those costs on to consumers — neither of which is ideal. Next, retailers need to standardize the intake process. This intake process helps retailers primarily in two ways: 1.

Less than five years ago, many consumers wouldn’t have heard of buy now pay later (BNPL). per cent) are now aware of BNPL services, overtaking traditional online payment platforms like Paypal, Visa and Western Union, according to Roy Morgan’s Digital Payments Report last year. Trust and the consumer.

A new study from FIS ® (NYSE: FIS), shows how the shopping preferences of younger UK consumers have shifted as adoption of embedded financeservices reaches mainstream usage among Millennials and Gen Zs, while their older counterparts are less engaged with newer, digitally-oriented financial experiences.

But the direct-to-consumer (DTC) brand has other big goals, especially as many brands in its orbit assess costs and find ways to maintain profitability. Everyone has a different role in the process, but the goal is to execute the best we can to drive traffic and conversion.” That’s where Loren Simon comes in.

So what about first-party consumer data? Who is helping consumers access and use their own data? Consumers Want Control of Their Data. Consumers are seeking access, privacy and control over their data. Consumers are comfortable with data if they have access and if it proves its value. The Value in Receipt Data.

NatWest Group has signed agreements with three payment providers – TrueLayer, GoCardless and Crezco – to offer Variable Recurring Payments (VRP) as a new and convenient payment option for businesses and consumers.

Ecommerce and payments solution Digital River has added a new pay-later option for its U.S. Pay in 4 with PayPal allows customers to pay for purchases between $30 and $600 in four interest-free payments, while the merchants get paid in full up front. Consumers want to spend their own money.

New customers are a major growth engine for retailers, but many merchants view first-time online shoppers as high-risk due to their unfamiliar behaviour and lack of purchase history. Our data already shows that across the e-commerce landscape, up to 70 per cent of orders that are declined by merchants are made by legitimate customers.

But ongoing pressure from consumers, employees and even regulators has forced businesses — especially retailers — to reprioritize sustainability along with broader corporate social responsibility (CSR) strategies. Consumer Demands Accelerate Sustainability Priorities. of purchases.

Shopback’s decision to terminate its buy now pay later (BNPL) service in Malaysia and Singapore has sparked discussions and raised pertinent questions about the future of digital payment solutions in the region. For merchants, it means increasing basket sizes, which makes it a win-win situation for all involved,” he opined.

“Point of sale financing has historically been reserved for large purchases like luxury electronics, but now we are seeing an uptick in consumers using installment plans for smaller purchases across large and small retailers.” BNPL loans allow shoppers to make purchases with deferred or no interest installment loans.

For many consumers, online shopping is a reflex, which is a major boon to retailers of all shapes and sizes. As content increasingly moved online, the cracks in this process became ever more obvious. In short, the process of maintaining website content was extremely challenging, confusing and labor-intensive.

We organize all of the trending information in your field so you don't have to. Join 40,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content