This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Consumers now prefer digital payment options, with cash usage declining in all major economies. Cards have become by far the most popular payment method, with contactless now accounting for most purchases made at retail stores. That is why resilience is so crucial.

The Consumer Financial Protection Bureau (CFPB) has sued Walmart and Branch Messenger , alleging that the partners forced the third-party delivery drivers in Walmarts Spark Driver program to use costly deposit accounts to access their earnings and in the process harvested more than $10 million in fees from the workers.

As the holiday shopping season approaches, retailers face increased pressure to facilitate a seamless and secure shopping experience. Payments technology is central to the shopping experience. Innovations like biometrics and tap-to-pay have transformed how, when and where consumers shop.

The growing adoption of blockchain technology has created new opportunities for businesses looking to integrate digital assets into their operations. What is CaaS in Crypto and What Companies May Need This Service? These services typically include crypto payment gateways, digital wallets, and blockchain-based financial tools.

The adoption of cryptocurrencies has expanded beyond investment and trading, with businesses worldwide integrating crypto payment gateways into their operations. A crypto payment gateway allows merchants to accept cryptocurrency payments from customers, offering an alternative to traditional fiat transactions.

consumers abandon a purchase and stop accessing an online service because they can’t remember their passwords 4.76 Passkeys, another passwordless authentication method, leverage biometrics or a PIN to let consumers confirm a purchase with just a tap or a quick selfie. times per day on average.

Over the past decade, the payments environment has experienced significant upheaval, driven by swift technical improvements. Innovations such as contactless cards, mobile wallets, blockchain, and real-time payments are transforming transaction methods for consumers and companies.

that, together, process millions of returns every month. has nearly doubled over the last six years, now accounting for roughly 17% of all merchandise sold, according to Timothy Fehr, COO of Happy Returns, citing research conducted in partnership with the National Retail Federation. The rate of goods returned in the U.S.

Using our payment card whilst we shop online rarely gives us pause, and the many millions who buy online generally trust the system. However, the recent busy shopping season means it’s a good time to remind ourselves that there is an ongoing battle to make sure that the payment card data of your customers remains secure.

A recent study found that three-quarters of consumers will avoid a brand after a cybersecurity issue, and more than 40% assume that brands are to blame when an incident occurs. Another survey of online consumer attitudes found that 84% wont go back to an ecommerce site after a fraud experience there.

If we thought the pandemic-driven shift to digital payments was an evolution, we’re about to be catapulted into a new world, where payments will become possible in places thought impossible just a few years ago. Currently, consumerpaymentsaccount for more than 60% of all embedded finance transactions and are set to reach $3.5

3D Secure (3DS) is an additional layer of cardholder security and authentication for online card transactions, and more and more large retailers are wanting to add it into their paymentsprocess. This not only expedites processing for legitimate customers but also more accurately flags fraudulent charges.

No matter how fast the modern payment ecosystem is developing, the pursuit of the best customer experience isn’t going anywhere. To answer customers’ demands, business leaders must find the balance between adapting services to consumers’ digitally-driven shopping behaviors and staying true to the company’s strategy.

The increase in social media usage, combined with a tandem increase in online purchasing, proved to be the push both consumers and brands needed to move into the burgeoning realm of social commerce. after Google, accounting for 25.2% Trust Plays a Big Role in Consumers’ Willingness to Shop on Social.

Fraud has plagued retailers for quite some time, but the issue is now getting its time in the spotlight due to the increased use of AI within the industry, as well as consumers’ general awareness of the trend. This is a more straightforward use case for AI implementation, and one that consumers have come to know and crave.

Once, borrowing money to make a purchase was a relatively tedious process, not a spur-of-the-moment thing. In recent years, though, the financial technology or fintech revolution in the customer credit market has changed all that, with the meteoric rise of buy-now-pay-later (BNPL) services. But does it also change our spending habits?

New account fraud is surging, and despite the conventional wisdom that this type of fraud is mostly a problem for banks, retailers are in the crosshairs too. In fact, account creation fraud rates are growing fastest in the retail sector, with 44.7% Data breaches have been a problem for many years, but 2023 was the worst yet for U.S.

Businesses today operate in a fast-moving cyber threat landscape. As digital operations become more complex and cybercriminals launch increasingly sophisticated phishing and malware attacks, data breaches have become common occurrences. For retailers and consumer businesses, a surge in data breaches presents difficult challenges.

That inherent distaste for the transaction phase is one reason payment companies are so eager to expand into other parts of the shopper journey. taking place online, digital payment solutions like Venmo and PayPal (which has owned Venmo since 2013) are well positioned to capitalize on the opportunity.

In 2023, fraudulent returns accounted for a staggering 13.7% With the rise of ecommerce, direct-to-consumer (DTC) retailers are particularly vulnerable as their online-only presence provides fertile ground for fraudulent activities. Refund fraud is a significant issue for U.S. retailers, costing billions of dollars annually.

As their popularity continues to surge, it is crucial for retailers to consider embracing crypto acceptance as a payment option. There are a number of businesses across Australia already accepting cryptocurrency payments. Mitigating the volatility of cryptocurrencies can be a barrier for retailers as a payment option.

The Consumer Financial Protection Bureau (CFPB) has issued an interpretive rule confirming that buy now, pay later (BNPL) lenders are in essence credit card providers, meaning they will be required to provide consumers with legal protections and rights, including in cases of disputed charges and issuing refunds. 1, 2024.

To safeguard profits, protect customers, and maintain operational stability, retailers must proactively address these challenges with modern solutions. Retail risk encompasses any potential threat that could disrupt a stores financial health, reputation, or daily operations. In 2024, the average cost of a data breach reached $4.88

The lawsuit, filed in 2017, alleged that Founder and then-CEO Kevin Plank knowingly or recklessly misrepresented facts regarding consumer demand for Under Armour’s products as well as the company’s financial and operating results, according to the Wall Street Journal. 16, 2015 and Nov. billion revolving credit facility.

Walgreens has introduced the myWalgreens Credit Card program, while supermarket chain Giant Eagle will start accepting PayPal and Venmo in-store as retailers continue expanding their payment options. The move also can speed up paymentprocesses via PayPal and Venmo QR codes.

These devices, like smart doorbells, thermostats, lighting and more, present an exciting opportunity for retailers, but understanding consumers motivations and proactively addressing potential concerns will be vital to make the most of this dynamic market. Craig Thole is SVP of Emerging Solutions, Global Connected Living, at Assurant, Inc.

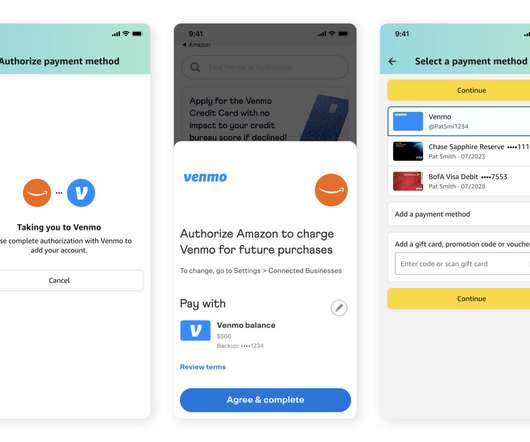

Amazon will begin offering Venmo as a payment option on its website and app, rolling it out to select customers immediately and available to all U.S. Amazon shoppers will be able to add their Venmo account as a payment method for their Amazon account and even set it up as their default payment option.

Australia will create a licencing framework for cryptocurrency exchanges and consider launching a retail central bank digital currency as part of the biggest overhaul of its payments industry in a quarter of a century. “Australia must retain its sovereignty over our payment system.”

And it’s increasingly clear that brands that embrace financial services within the customer journey are scoring highly on engagement scores. What’s more, the number of payment providers on the market has dramatically multiplied over the years, creating a vast and often confusing ecosystem. It’s reckoned that nearly 4.5

Consumers are quickly losing trust, and companies must act swiftly and responsibly to restore it. A Pew Research study reveals a concerning trend: 67% of consumers have little understanding of what companies do with their data, a sentiment echoed by an IAPP study which found that only 29% feel informed about how their data is protected.

Once, borrowing money to make a purchase was a relatively tedious process, not a spur-of-the-moment thing. In recent years, though, the financial technology or fintech revolution in the customer credit market has changed all that, with the meteoric rise of buy-now-pay-later (BNPL) services. But does it also change our spending habits?

Sika Health — a payment solution that enables ecommerce merchants to accept Health Spending Account (HSA) and Flexible Spending Account (FSA) payments — has launched a new marketplace where consumers can shop directly for HSA- and FSA-eligible products.

The numbers currently used to identify cards will be replaced with tokenisation and biometric authentication In 2022, Mastercard added biometric options enabling payments to be made with a smile or wave of the hand. Credit card numbers and payment details are often exposed in major data breaches affecting large and small businesses.

“Mobile technology is transforming payments, making it easier, safer and more affordable for people to move and manage their money than ever before,” said Dan Schulman, President and CEO of PayPal at the time of the spinoff. “As Consumers are now more digital, and they’ve gotten into these habits. Source: CivicScience.

The digital wallet will be managed by Early Warning Services (EWS) , the company that operates Zelle, but will operate separately from Zelle. The other four owners in the EWS/Zelle venture include Capital One Financial , PNC Financial Services Group , U.S. By 2025, digital wallets are expected to account for 52.5%

Options such as buy now, pay later (BNPL) services were first introduced to business to consumer (B2C) transactions, giving customers the ability to access products and services they need today while paying at a later date or over a series of instalments. . Transform your B2B transactions with better payment technology.

So-called “negative option” services are a controversial yet time-tested method of doing business. Under this model, a customer signs up for a subscription service, typically as part of a free trial offer. The customer is then charged on an ongoing basis unless they explicitly cancel the service in question.

Australian retailers remain vulnerable to the slowdown in consumer spending and rising living costs, say retail lobby groups, in a subdued response to the Federal Budget. Addressing unfair, excessive card surcharges, including preparations to ban debit card surcharges, which will deliver lower-cost payments.

The INFORM (Integrity, Notification, and Fairness in Online Retail Marketplaces) Consumers Act, which went into effect in late June 2023, marks a significant step forward in curbing online fraud by third-party sellers and organized theft from retail stores. But compliance can be complicated. Freeze non-compliant seller accounts.

The pandemic accelerated not just ecommerce but also digital payment methods: digital wallets reached 29.3% The wallets are expected to unseat credit cards as the preferred online payment method in the coming years, according to the FIS Global Payments Report 2021. Digital wallet usage is expected to account for 40.5%

billion on pet food and treats, supplies, medicine, vet care and other services in 2022, and are predicted to spend $143.6 Myos Fetch is a full-service SMS “concierge” for all things related to the brand and its focused, yet growing, product line. More than 66% of U.S. million or so homes spent $136.8 billion in 2023.

It’s clear this reverse layaway payment model is also here to stay. In BNPL, consumers receive the goods or services that they want to buy, but payment is staggered over monthly payments for a certain period of time with no interest. It’s not hard to understand the appeal.

The campaign, which ran from January 2020 to August 2021, was for a 60-month interest-free and no-deposit payment method. According to the Australian Securities and Investments Commission (Asic), many consumers may have been unaware of the financial arrangements they entered when buying products at Harvey Norman stores.

The Consumer Financial Protection Bureau (CFPB) is planning to start regulating buy now, pay later (BNPL) products. Apparel and beauty companies accounted for 80.1% Buy Now, Pay Later is a rapidly growing type of loan that serves as a close substitute for credit cards,” said Rohit Chopra, Director of the CFPB in a statement.

We organize all of the trending information in your field so you don't have to. Join 40,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content